Insurance Companies Fuel the Climate Crisis

By Dom Altomari, March 26, 2026

Insurance companies are funding the fossil fuels driving climate disasters, then raising your premiums, denying claims, and dropping coverage when those disasters hit. You’re paying more for less protection, while they profit from the crisis on both ends.

Insurance companies–traditionally seen as protectors against risk–contribute to the very climate crisis they claim to protect their customers against. Major insurers such as Allstate,Chubb, Liberty Mutual, and AIG invest heavily in the fossil fuel industry while simultaneously raising premiums and withdrawing coverage from vulnerable communities due to increasing liabilities from climate-related disasters. These actions reveal a troubling truth that has plagued the insurance sector since as early as 1954.

Despite their public commitments to sustainability, insurers funnel vast amounts of funding into coal, oil, and gas projects. In the United States alone, insurers hold approximately $536 billion in fossil fuel assets as of 2019. Globally, 15 leading insurers invested nearly $7.9 billion in North Sea oil and gas ventures between 2019 and 2021, with European giants like Axa, Allianz, and Aviva contributing $4.6 billion in 2021. These investments enable fossil fuel companies to continue operations and expand projects, as insurance coverage is essential for managing the liabilities associated with pipelines, drilling rigs, and refineries. Without the backing of major insurers, many fossil fuel projects would become financially unviable.

Why is the insurance industry helping the climate crisis?

This financial entanglement results in a stark hypocrisy: insurers are increasing rates and refusing coverage in regions prone to disasters exacerbated by climate change, such as wildfires, floods, and hurricanes, while underwriting the very industries that drive these risks. Activists highlight this disconnect, pointing out that insurers exclude households in high-risk areas but continue to support fossil fuel expansion, effectively fueling the climate crisis with customers’ premiums. This also exacerbates the housing affordability crisis by driving up premium costs and making insurance less accessible in climate disaster-stricken areas.

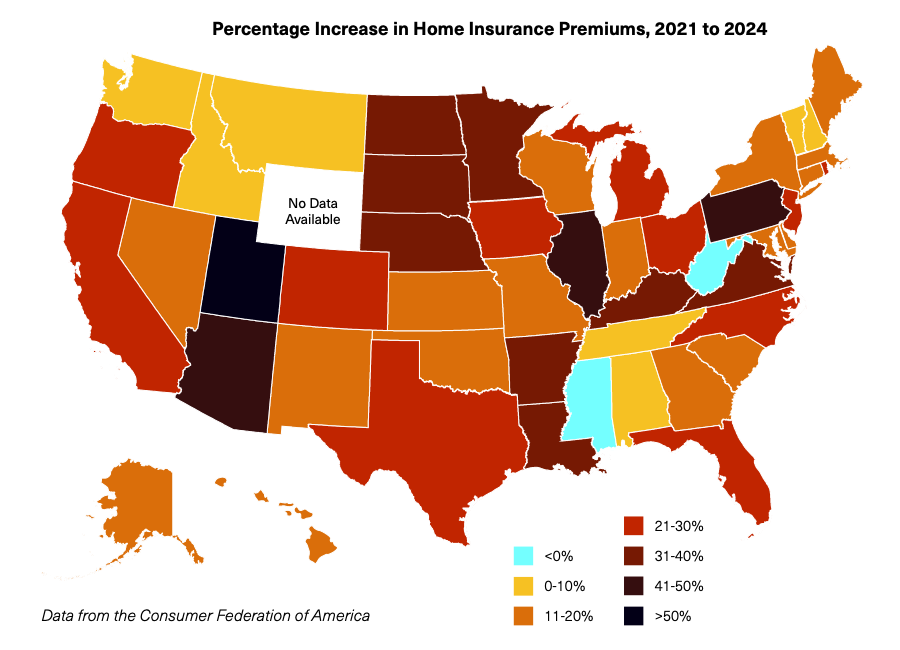

The consequences of this dynamic are evident in the rising costs and shrinking availability of insurance for homeowners. Climate change has intensified the frequency and severity of natural disasters, leading to record numbers of insurance claims and economic losses. The devastating California wildfires of January 2025 caused approximately $250 billion in damage, with insurers expected to pay out $40 billion, making it the largest wildfire insurance payout in history. Scientists estimate that climate change increased the likelihood of these fires by about 35 percent. In response to more and more claims being filed that insurance companies have to process, they’ve responded by hiking premiums, tightening policy terms, and withdrawing from high-risk markets in moments of peril.

From 2021 to 2024, average home insurance premiums in the U.S. surged by roughly 30 percent, significantly outpacing inflation. Many insurers have pulled out of hurricane-prone states like Florida and Louisiana altogether, while policy cancellations and non-renewals have left homeowners scrambling for coverage in wildfire-prone California. This phenomenon is known as “bluelining,” and disproportionately affects the communities most exposed to climate hazards.

Bluelining – Tackling an Emerging Climate Justice Issue

Further, insurers frequently deny or drop claims, leaving victims of climate disasters without financial relief. In Florida, for instance, State Farm denied nearly half of homeowners’ hurricane claims in 2022, impacting over 76,000 households. Meanwhile, top insurance executives continue to receive multimillion-dollar salaries, underscoring a disconnect between corporate profits and consumer hardship.

As private insurers retreat, the financial burden shifts to consumers and taxpayers. Many states operate “insurers of last resort” programs, such as California’s FAIR Plan, which absorbed a $1 billion reinsurance bailout following the 2025 wildfires. These programs, funded by policyholder fees and government support, carry the riskiest policies that private insurers increasingly reject. Rising insurance costs also contribute to higher mortgage payments and rents, amplifying economic strain across the population. A 2024 industry survey found that a staggering 12% of Americans no longer have home insurance, up from 5% in 2019. Lower-income families bear the brunt of this crisis, as they are more likely to be uninsured and thus suffer total losses without support. In California, affordable housing developers have reported laying off staff and selling off rent-controlled properties to private landlords due to rapidly rising insurance costs, further exacerbating the dangers posed to low-income families.

On a more hopeful note, as more reports are published, awareness becomes impossible to hide and calls for accountability and reform grow louder. Advocates are urging insurers to recognize climate change as a direct financial risk linked to fossil fuel emissions, and to hold polluters accountable through legal and financial mechanisms. Proposals include requiring insurers to subrogate against major emitters to recover disaster-related costs, ending all financial support for fossil fuel industries, and adjusting insurance pricing to reflect clients’ carbon footprints and mitigation efforts. Some states, including Hawaii, California, and New York, are exploring legislative options to shift the financial responsibility for climate damages onto fossil fuel companies.

Despite public pledges to achieve net-zero emissions, many insurers have been found guilty of greenwashing as their continued investments and insurance coverage of fossil fuel projects contradict their stated climate goals. A decisive step insurers could take is to refuse coverage for any new coal, oil, or gas ventures, effectively halting further fossil fuel infrastructure development. This action would leverage insurers’ unique position as gatekeepers of risk to drive critical and urgently necessary systemic change.

In fact, some insurance companies are already demonstrating that their role can evolve to support climate resilience infrastructure rather than undermine it. The Mesoamerican Reef in Mexico is a 700-mile stretch of coral reef and happens to be the second-largest barrier reef system in the world, playing a fundamental role in both the local ecosystem and the local economy. It is now insured as a valuable natural asset, marking a significant pioneering approach to conservation finance. The policy, which is backed by a collaboration between local governments, private stakeholders, NGOs, and insurers such as Swiss Re, provides rapid funding for reef restoration following storm damage, as was successfully tested after Hurricane Delta in 2020. This parametric insurance model enables prompt repair efforts critical to the reef’s survival, preserving its function as a natural coastal barrier that reduces wave energy by up to 97 percent, protecting local communities and economies reliant on ecotourism and fishing.

By assigning economic value to the reef’s ecosystem services, this insurance approach incentivizes the preservation of natural capital and creates a scalable framework adaptable to other ecosystems, such as mangroves, wetlands, and forests. Mangroves, for example, offer cost-effective protection against storm surges and flooding, with demonstrated benefits such as preventing $1.5 billion in flood damages during the 2017 Hurricane Irma in Florida. The model promotes public-private partnerships, with premiums funded by local hotels and government bodies, fostering shared responsibility for ecosystem health.

While challenges remain, like ensuring timely payouts and identifying willing payers for insurance coverage, this initiative signals a transformative shift in how the insurance industry can support climate adaptation and nature-based solutions. By integrating the protective value of ecosystems into underwriting and pricing, insurers can encourage conservation through financial incentives, potentially reducing premiums for clients who maintain healthy natural buffers to increasingly extreme natural disasters. This emerging role of insurance not only counters the industry’s historical complicity in fossil fuel financing but also exemplifies how insurers can leverage their unique position to foster systemic change, aligning financial flows with urgent climate goals and the protection of vulnerable communities.

Source: Center for Climate Integrity

It is clear that the insurance industry currently operates at a crossroads, profiting from underwriting fossil fuels while the costs and assumed liabilities of climate disasters continue to skyrocket. Already, climate-related damages are costing the global economy an estimated $16 million per hour. The United States now spends nearly a trillion dollars every year to recover from the impacts of climate change. These expenses increasingly fall on homeowners and taxpayers, while fossil fuel companies continue to reap profits. Without a fundamental shift in insurer practices, such as divesting from fossil fuels to invest in natural assets and demanding accountability from polluters, the current path leads toward an uninsurable future marked by unprecedented climate disasters, ecosystem destruction, rising premiums, denied claims, and widespread economic hardship. The insurance industry must leverage its power to take urgent action and align financial flows with the dire need to reduce greenhouse gas emissions, protect vulnerable communities, and ensure a livable planet for future generations.

Take Action

Public advocacy is our most critical line of defense. Here are ways that you can take action to hold insurance companies accountable for their role in exacerbating (*or should it be fueling) the climate crisis:

Sign on to Action Network’s petition demanding insurers “stop funding climate change.”

Check out the campaigns being done by Insure Our Future and get involved.

Find out if your insurer is supporting fossil fuels and transition to a responsible alternative.

Write a letter to major insurers AIG and Chubb today to demand they stop enabling fossil fuels, respect human rights, and support a just clean energy transition.

Tell State Leaders to Pass the Fossil-Free Insurers Act.

Sign Stop the Money Pipeline’s petition demanding “Wall Street and Congress: Put People Before Polluters.”

Sign the petition by Rainforest Action Network to “demand Chubb insure our future, not fossil fuels.”

If you are a current student, you can take action with Insure Our Future.

Californians, email your senator and encourage them to vote for Senate Bill 222, the Affordable Insurance and Climate Recovery Act.

Change the Chamber is a nonpartisan coalition of young adults, 100+ student groups across the country, environmental justice and frontline community groups, and other allied organizations. To support our work, donate or join our efforts!